Housing Starts Up In February

By 250 News

Prince George, B.C.- Canada Mortgage and Housing is reporting another strong month for housing starts in B.C.

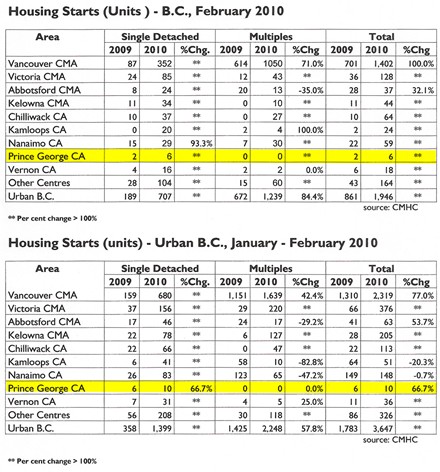

In Prince George, there were six homes started last month compared to just 2 started in February of 2009.

CMHC says there is still a need to be cautious however, as these increases should not be overstated. The first few months of 2009 saw some of the lowest levels of homebuilding on record, so year-over-year comparisons are large.

Home starts this year are forecast to be higher than 2009 but below the five-year average.

“We are on our way back to healthy levels of new home construction in line with homeownership demand,” noted Robyn Adamache, Senior Market Analyst at CMHC.

Provincial home starts in urban areas increased to 26,900 units, seasonally adjusted at annual rates (SAAR) in February, from 24,900 in January.

At the national level, total housing starts rose to 196,700 units SAAR in February from 185,400 units a month prior.

Previous Story - Next Story

Return to Home

These rules will raise the gross amount of income required to qualify, depending on the term.

And look for higher interest rates soon as well.

That will be a problem for a lot of people.

This in itself isn't a bad thing as such,but it will affect housing sales.

The realtors will not be happy and the banks will be much tougher to deal with.

CMHC is also going to be harder to deal with.

They are already designating certian areas with a high foreclosure rate due to unemployment and loss of jobs,as high risk.

No more grey areas.

It is going to get tougher to buy a home.